Working Capital is a key component of every M&A transaction so it is important to understand what role it will play in the sale of your company.

First, let’s start with how transactions are typically structured:

Transaction Structure

Most acquisitions of mid-sized companies are structured on a Cash Free / Debt Free basis with a Working Capital adjustment:

- Cash Free – The seller keeps the cash in the business (cash is excluded from the transaction).

- Debt Free – The seller pays off all bank debt such as term loans or lines-of-credit.

- Working Capital Adjustment – The buyer receives an agreed upon amount of working capital on the day of closing.

The first two deal points are fairly self-explanatory. The last point, working capital, is more complicated and less understood.

What is Working Capital

Working Capital is the difference between the company’s current assets and the current liabilities. It is a reflection of the capital (money) employed in the business to support the ongoing operations. The primary current assets (excluding cash) in most businesses are accounts receivable and inventory; and the primary current liabilities are accounts payable. In addition, there are often other smaller categories of current assets and current liabilities that are included in working capital.

Buyers view working capital as an important operating asset of a company. When a buyer makes an offer to purchase a company, they expect to receive all of the operating assets in the business which includes an appropriate amount of working capital.

Calculating Your Company’s Working Capital

To calculate your company’s working capital:

- Add the accounts receivable, the inventory, and the other current assets; then

- Subtract the accounts payable and other current liabilities.

Since cash is generally excluded from the transaction it is not included in the working capital calculation. Also, some accrued employee liabilities (such as accrued payroll and PTO) are the seller’s responsibility to pay off at closing, so they are also excluded from the calculation.

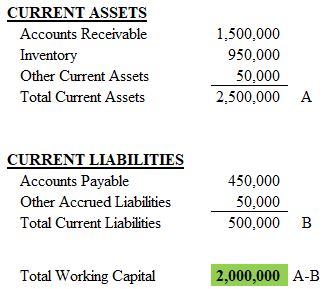

Here is an example of how to calculate working capital:

In the above example the company has $2.5 million of current assets and $500,000 of current liabilities resulting in working capital of $2.0 million.

Establishing a Working Capital “Target”

The working capital Target is the amount of working capital that must be in the business on the day of closing. The Target is agreed to by the buyer and the seller and should reflect an amount that is consistent with historical operations. Since a company’s working capital fluctuates from month-to-month, agreeing on the Target is often a challenge with both the buyer and seller having different opinions on the appropriate amount. Although there are numerous ways to determine the Target, one of the most common methods is to use the average working capital over the twelve months prior to closing. If there is a high degree of seasonality in the business this should be taken into account as well.

Closing Day Working Capital Adjustment

The night before the transaction closes the seller will prepare an estimated closing day balance sheet which will be used to calculate the actual closing day working capital. The closing day working capital will be compared to the Target, and there will be a dollar-for-dollar adjustment to the purchase price for the amount that the closing day working capital is higher or lower than the Target. For example, if the Target is $2 million and the actual is $2.1 million then there will be a $100,000 increase to the purchase price. The same adjustment would be made on the down side if the actual was less than the Target.

The purpose of the working capital adjustment is to keep the deal fair for both the buyer and the seller through the closing process. It ensures that the buyer will receive a sufficient amount of assets on the day of closing. It also protects the seller from wide fluctuations in working capital and provides for additional consideration if working capital exceeds historical averages.

Want to learn more about working capital or any other topic related to deal structures? Give us a call or send me an email: SCOTT@CENTERPNT.COM . We’d love to hear from you.